Date: January 17, 2025

Author(s): Evelyn Blumenberg, Samuel Speroni, Fariba Siddiq, Jacob L. Wasserman

Abstract

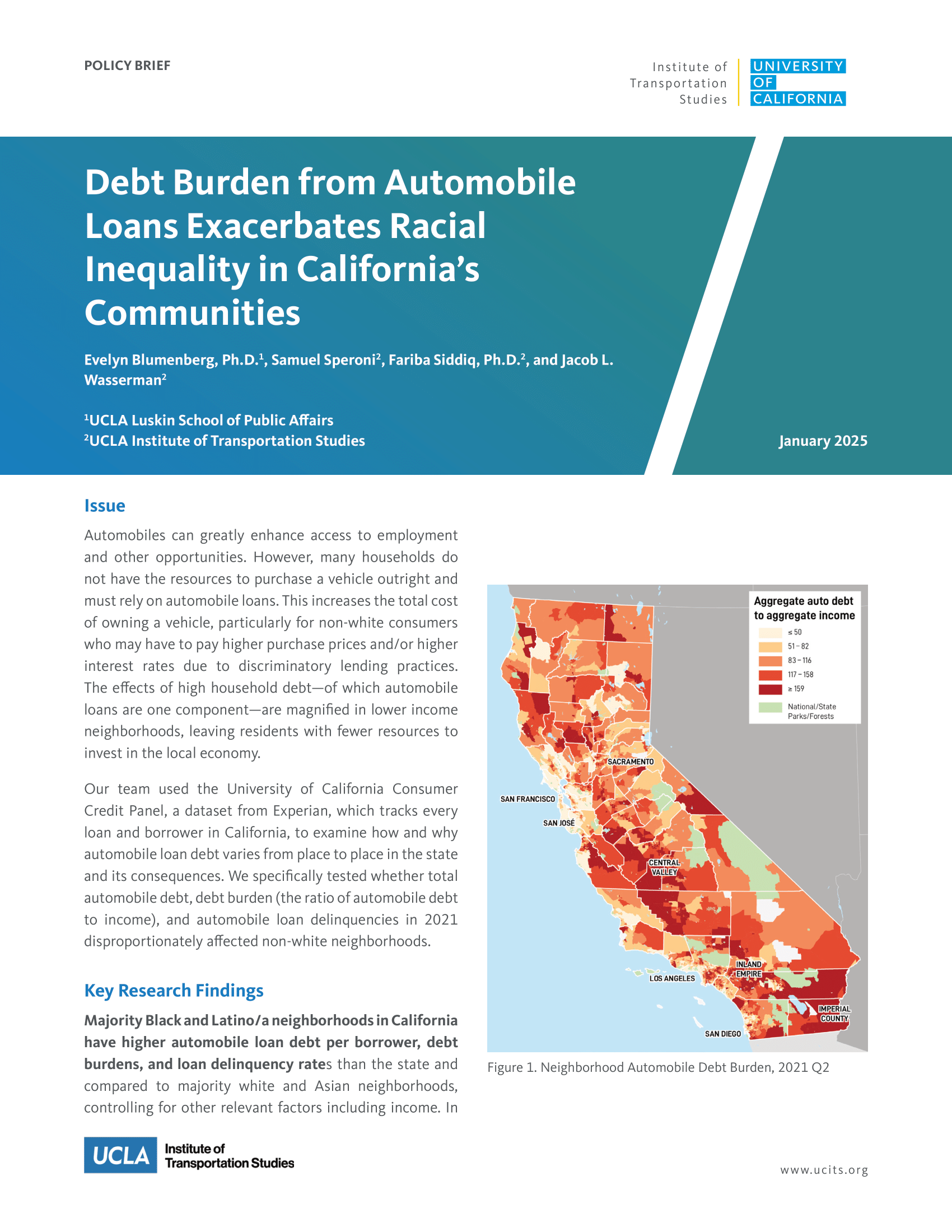

Automobiles can greatly enhance access to employment and other opportunities. However, many households do not have the resources to purchase a vehicle outright and must rely on automobile loans. This increases the total cost of owning a vehicle, particularly for non-white consumers who may have to pay higher purchase prices and/or higher interest rates due to discriminatory lending practices. The effects of high household debt—of which automobile loans are one component—are magnified in lower income neighborhoods, leaving residents with fewer resources to invest in the local economy. Our team used the University of California Consumer Credit Panel, a dataset from Experian, which tracks every loan and borrower in California, to examine how and why automobile loan debt varies from place to place in the state and its consequences. We specifically tested whether total automobile debt, debt burden (the ratio of automobile debt to income), and automobile loan delinquencies in 2021 disproportionately affected non-white neighborhoods.

About the Project

Most U.S. metropolitan areas developed alongside the automobile. Consequently, access to opportunities in these neighborhoods is predicated on having an automobile, yet many households do not have the resources to purchase one outright, relying on automobile loans to spread out the purchase price. Moreover, COVID-19 altered travel patterns in the U.S. Few studies have focused on automobile ownership—a relationship with potentially long-term consequences for accessibility, household budgets and debt, and policy efforts to meet climate goals. To understand the association between the pandemic and automobile ownership, this project first examines three different automobile loan-related outcome measures: annualized growth rate of new automobile loan balances, average new loan size, and the number of new loans. The annualized growth rate of new automobile loans increased during the pandemic across all neighborhoods by race/ethnicity, increasing most rapidly in Latino/a neighborhoods. Controlling for other factors, loan size increased similarly across neighborhoods by race/ethnicity. The increase in automobile lending in Latino/a neighborhoods, therefore, likely was explained by a significant uptick in the number of new loans. The growth in automobile lending during the pandemic was potentially prompted by pandemic-induced changes in the need for automobiles and facilitated by an expanded social safety net. Second, the project explores the determinants and geography of automobile debt and its consequences in California, testing whether various automobile debt measures disproportionately affect non-white neighborhoods. Controlling for other factors, Black and Latino/a neighborhoods have higher total automobile debt, debt burdens (debt relative to income), and automobile loan delinquency rates. The findings underscore the importance of policies to offset the costs of automobile ownership and access.